Payroll Earnings Update Jan 2024

Payroll Earnings Update Jan 2024

ADP, Paycom, Paychex, Paycor, Dayforce (fka Ceridian), Paylocity

Payroll and HCM providers continue to grow, with expanding margins, albeit at a slower pace.

Key Callouts

New Products - Paycom and Dayforce (fka Ceridian) are transitioning into new product rollouts that impact pricing, margin, and retention.

Softening Retention - Paycom is seeing slowing customer growth, worse retention, but industry high gross margins.

Generative AI features - ADP announced new Generative AI features.

Multiples compression - Multiples continue to compress despite growth.

Clear market segment positioning - Market positioning and product differentiation between the companies is clear.

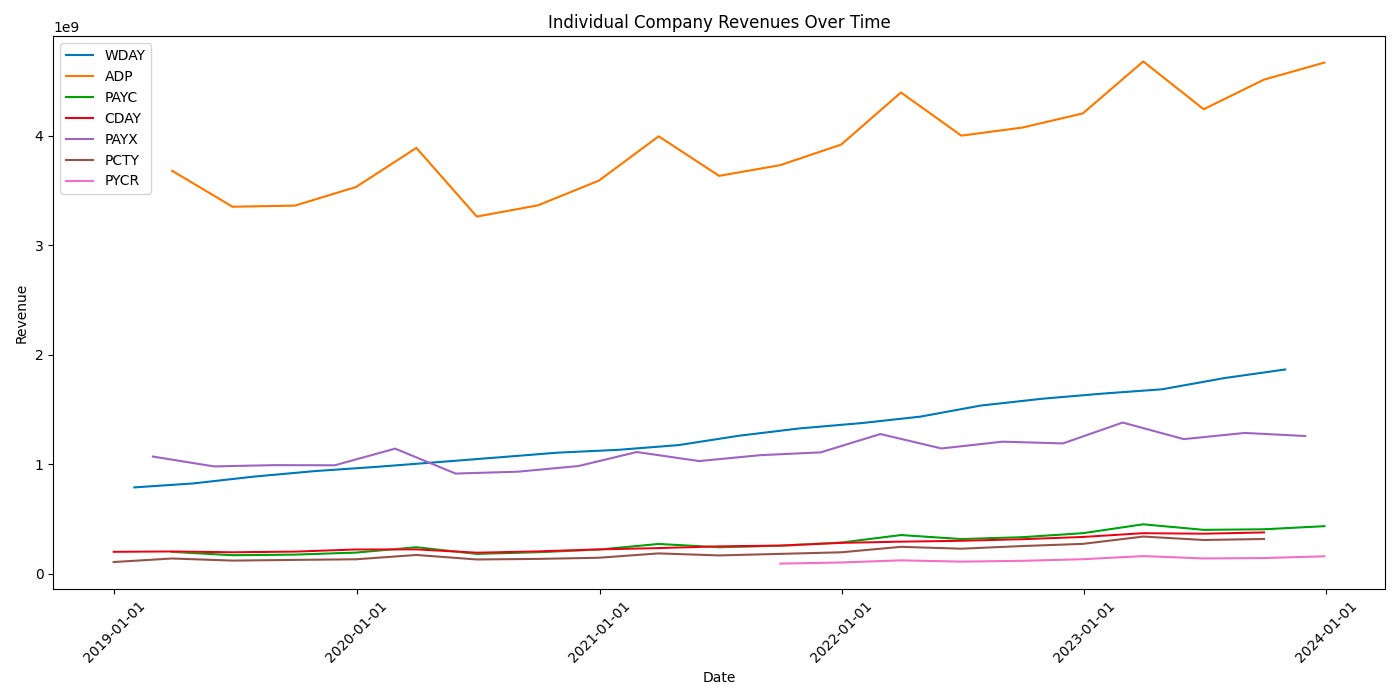

Year-on-Year Revenue Growth

Paycom: +23%

Paychex: +20%

Dayforce: +18.9%

ADP, Paychex: +6%

Paylocity: +16%

ADP is by far the largest company, seeing the slowest growth, no surprise.

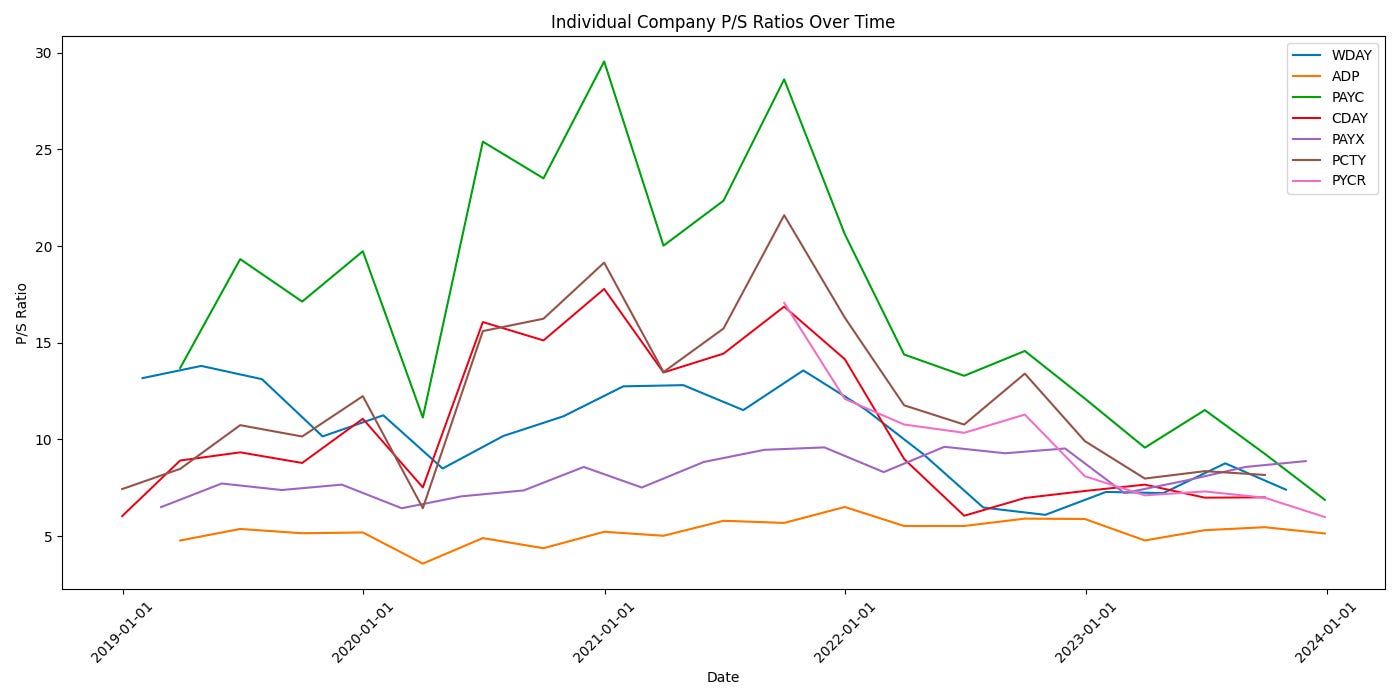

Multiples are compressing

Despite revenue and margin growth, stock multiples continue to compress. The interest rate change period is obvious in this graph, but multiples are still moderating downward even as interest rates have stayed stable. This reflects concerns about the future economic conditions, particularly as it impacts payroll (high number of layoffs is certain industry segments).

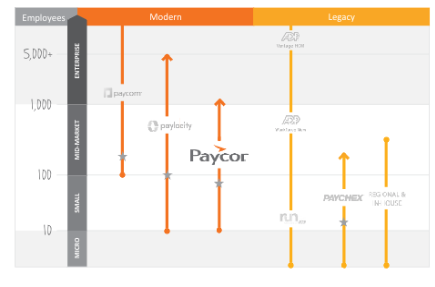

Company vs market positioning

Software payroll providers are still eating up market share from legacy, regional providers, either software or person based. Each one of these companies has defined specific areas they are going after, tailoring their suite to serve those needs (note: Dayforce is largely targeting multinational corporations).

Paycom’s struggles with Beti: revenue and retention

Paycom’s stock melted down after earnings updates related to ‘Beti’. Beti improved user experience, reduced errors, but also reduced payroll runs to “fix” payroll errors. Paycom charges on a payroll run basis, thus reducing earnings. Despite those issues, Paycom’s *gross* margins are higher than the other industry participants by a lot:

Gross margins:

Paycom: 86.7%

Paychex: 71.5%

Paylocity; 69%

Paycor: 66%

ADP & Dayforce: 47%

This partially reflects revenue mix, for example ADP includes Professional Employer Organizations and other business lines, but does show higher monetization on Paycom’s end.

Paycom retention is decreasing, moving from 91% to 90% (not a good number). Paycom claims this reflects Covid era efforts to recruit small businesses that churn off at higher rates. In general, net revenue retention for most software companies has decreased year-on-year because of covid era *high* NRR due to expansions. It’s possible, but Paycom’s stock shows the worst performance of the group over the past 1 and 3 year periods of time.

Generative AI is not a big focus for payroll companies

ADP has been the most ambitious about innovation and Generative AI. It rolled out ADP Ventures and ADP Assist last quarter.

Other payroll providers are focused on more traditional AI and decision systems to improve user experience.

The payroll market is seeing continues growth and decent margins, but churn from worsening labor markets are an overhang.